How Property Tax Works

Geauga County Auditor Chuck Walder explained the basics of Ohio’s property tax system during a March 10 forum on property tax abolition.

Geauga County Auditor Chuck Walder explained the basics of Ohio’s property tax system during a March 10 forum on property tax abolition.

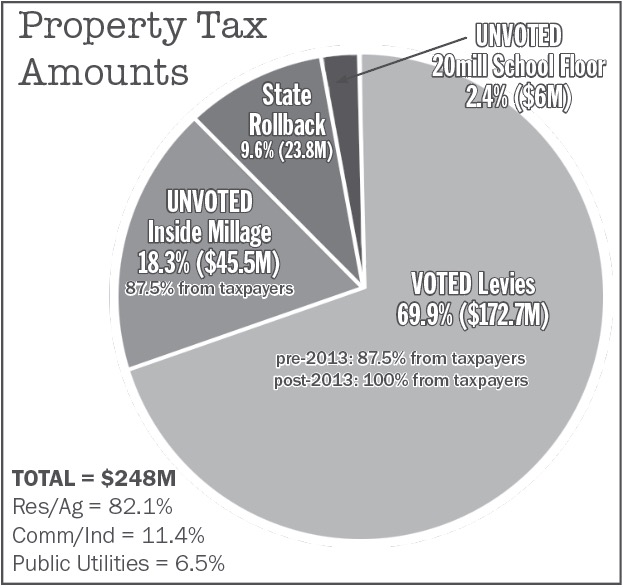

A typical property tax bill has three primary components, Walder said: inside millage, which accounts for about 18% of the bill; outside millage, which makes up roughly 70%; and the 20-mill floor, which does not apply to all taxpayers.

Inside millage is an unvoted component capped by law at 10 mills. Under the Ohio Constitution, that revenue is divided among local governments. About 45% percent goes to the local school district, 30% goes to the township, village or city where the taxpayer lives and 25% goes to the county.

“That particular number moves proportionally with valuation of your property,” Walder said. “So, as your property values go up, if they go up 10%, theoretically, the inside millage goes up 10%.”

However, House Bill 335, which goes into effect this year, will limit the growth of inside millage to inflation, he said.

Outside millage consists of voter-approved levies. Unlike inside millage, those values do not change when property values rise or fall, Walder said.

However, taxes can shift through a process known as tax equalization, he said.

For example, if two houses are valued the same, but one property’s value increases during a revaluation while the other decreases, the tax burden may shift from one property owner to the other, Walder said.

House Bill 96, which passed last year, eliminates the ability for entities to place replacement levies on the ballot and will affect this component of the system, he said.

There are also two key elements within outside millage, he noted. Levy funding approved before 2013 receives “rollback” credits from the state, while levies approved after 2013 are fully paid by the taxpayer.

The 20-mill floor is another unvoted component intended to ensure a minimum level of school funding. According to a document from the auditor’s office, the provision adjusts tax rates within a school district to 20 mills if the calculated floor millage falls below that level.

House Bills 129 and 186 will also take effect this year and will include previously excluded levies in the floor calculation while limiting increases to the 20-mill floor to the rate of inflation, the document said.