Vetoes, potential overrides and the effects of House Bill 96 on Chardon Schools were key topics of discussion during the July 8 meeting of the Chardon Schools Board of Education.

Vetoes, potential overrides and the effects of House Bill 96 on Chardon Schools were key topics of discussion during the July 8 meeting of the Chardon Schools Board of Education.

Gov. Mike DeWine signed House Bill 96 — the state’s operating budget for fiscal years 2026-2027 — into law on June 30, issuing 67 line-item vetoes in the process.

The board, which previously expressed concern over changes in House Bill 96 affecting how school districts manage finances, met to review what was vetoed, which vetoes might be overridden and the possible implications for the district.

A primary concern for board members centered on Ohio’s school funding formula. Now in the fourth year of a six-year phase-in, the formula did not receive updates to its base cost inputs.

One new feature introduced in the bill is a performance-based supplement for high-achieving districts like Chardon, said Superintendent Mike Hanlon, who noted that most of the increases the district received from the bill are tied to that supplement.

“One of the curious things that was done is the supplement was carved out and kept outside of the (school funding formula), outside base cost funding,” Hanlon said.

“So, it basically makes it a stand-alone supplement and it doesn’t help the formula moving forward,” he added.

According to the board’s presentation, the budget also includes a base funding supplement of $27 per student in 2026 and $40 per student in 2027.

Although the final version of the budget continues to phase in the formula, it does not update the base cost inputs, resulting in the state’s share of public-school funding dropping to a historic low, Hanlon confirmed July 14.

The board had previously expressed concern that House Bill 335 — which eliminates inside millage for entities other than townships — might be used to reconcile differences between the Ohio House and Senate versions of the budget, but that did not happen, Hanlon said at the meeting.

Chardon Schools will receive more funding than the previous year, Treasurer Deb Armbruster said.

Still, Hanlon expressed frustration with the legislative process.

“The complicating part, from my perspective, having worked so closely with school funding, is these funds could have been directed through the formula and accomplished the same goal the legislature has. They chose not to do that,” he said.

Putting that money through the formula wouldn’t have completely solved the funding issue, he said, but would have put it closer.

Vetoes and Potential Overrides

Among the line-item vetoes issued by DeWine was a proposed 40% cash carryover cap, which would have limited a district’s carryover balance to 40% of its previous year’s general fund expenditures, Hanlon said.

This cap, he explained, would have forced districts to go to taxpayers more frequently for levies in order to stay under the cap while maintaining necessary revenue.

Other vetoes included provisions to count incremental growth levies, conversion levies and the property tax portion of combined levies toward the 20-mill floor, Hanlon said.

DeWine also vetoed a measure that would have made school board races partisan.

Hanlon explained that line-item vetoes can be overridden by a three-fifths vote in both the House and Senate, and such overrides can happen at any point over the next two years.

He noted the Ohio House appears poised to attempt several overrides on July 21.

Likely override targets include provisions allowing county budget commissions to reduce property taxes; the inclusion of emergency, substitute, incremental growth and conversion levies, along with combined school district income tax and property tax levies, in the 20-mill floor calculation; and the elimination of replacement, fixed-sum emergency and substitute emergency levies, Hanlon said.

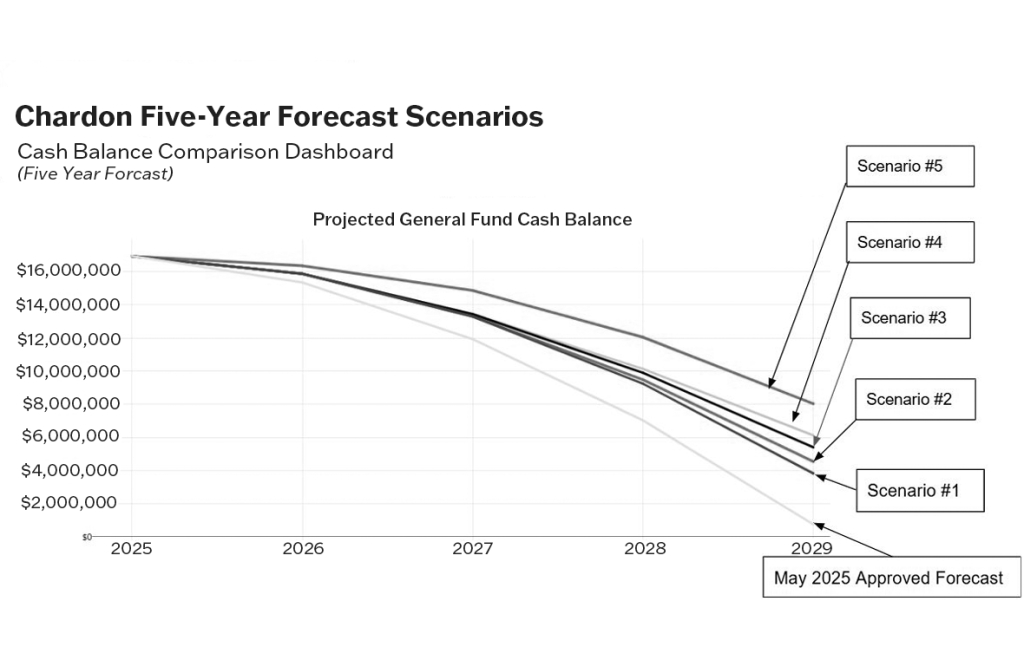

Financial Projections

Armbruster presented five different scenarios showing the potential impact of the budget bill through 2029.

Hanlon emphasized all projections are preliminary and should be considered just ideas being thrown around.

He also reminded the board the current state budget only covers fiscal years 2026 and 2027, and the district cannot predict what will happen in 2028 and 2029.

Armbruster said the district’s five-year forecast currently projects a levy in 2028. She noted that the district’s projected cash carryover percentage remains under 40% in all scenarios.

With the funding adjustments included in the budget bill, the school anticipates receiving an additional $468,106 in performance funding in 2026 and $272,650 in 2027, Armbruster said. She did not model any additional increases for 2028 or 2029.

Under the original forecast, the district’s general fund ending balance in 2029 was projected at $741,520. With the budget adjustments, that number rises to $3,808,677, Armbruster said.

Despite that increase, a levy is still projected for 2028, she said.

In March 2023, the board approved diverting 1 mill of general fund revenue to the permanent improvement (PI) fund, meaning it must be used for long-term capital projects.

Armbruster said if half of that mill were redirected back to the general fund beginning in 2027, the district’s 2029 ending cash balance would increase to $4,524,927 and the projected levy would be delayed to 2029.

Board President Karen Blankenship noted the need to assess how capital projects would be affected by pulling funds from the PI fund.

Another scenario involves phasing student fees back in — which the district had recently eliminated.

That phase-in would begin at 25% in 2027 and reach 100% in 2029, Armbruster said. Doing so would further increase the ending cash balance for 2029 and push the levy later into that year — though not as far as 2030.

A final scenario combining the return of 1 mill to the general fund and the full reimplementation of student fees would push the levy into 2030 and result in a projected 2029 ending balance of $8,016,177, according to Armbruster’s presentation.

Board member James Midyette asked about the difference between Chardon and Berkshire schools regarding millage adjustments, referencing a recent controversial decision by the Berkshire Schools Board of Education.

Armbruster explained Berkshire’s move to shift millage from its general fund to its PI fund would have dropped the district below the 20-mill floor, which would have increased tax rates.

Chardon, by contrast, is significantly above the 20-mill floor, she said.

Armbruster added the district would need to act by December if it wants to pursue the final scenario.

Even if the vetoes are overridden, the district is in a very good spot financially, Armbruster said.

Hanlon said with student enrollment continuing to trend downward, the district might be approaching another reconfiguration.

He noted the previous reconfiguration resulted in substantial savings and said the district might need to consider taking a facility offline.

However, he emphasized that reconfiguration is not being recommended at this time.

It is just something on the radar, he said.